#Industrial Water Treatment Chemicals Market Growth

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has 411 employees.

Text

A Deep Dive into the Industrial Water Treatment Chemicals Market: Insights and Analysis

The global industrial water treatment chemicals market size is expected to reach USD 21.23 billion by 2030, registering a CAGR of 4.9% during the forecast period, according to Grand View Research, Inc. The growth is majorly driven by growing demand for freshwater and favorable regulatory support for water treatment.

High requirement for drinkable water across the world has surged demand for the chemicals that are utilized in cleaning. The environment is seriously endangered by company waste. Due to accelerating urbanization, a rising economy, and expanding industrial activity, freshwater is witnessing high demand.

The U.S. Environmental Protection Agency (EPA) establishes national standards to ensure that consumption by humans is safe while considering the country's available technology and associated costs. The Safe Drinking Water Act and its amendments set up the fundamental framework for safeguarding the solution used by public systems in the U.S. This law specifies the requirements for guaranteeing the security of the nation's municipal drinking supplies. Systems that regularly serve 25 or more people per day or that have at least 15 service connections are considered public drinking sources.

In response to COVID-19, the governments of the affected economies have resorted to lockdowns and social distancing that have impacted the global supply chains. Several manufacturing activities were suspended which in turn, to resulted in the decline in sales of oil & gas and other industrial products. Moreover, due to the supply disruption, the price of raw materials increased significantly which in turn, was followed by an increase in the cost of treatment chemicals.

Gather more insights about the market drivers, restrains and growth of the Industrial Water Treatment Chemicals Market

Industrial Water Treatment Chemicals Market Report Highlights

• Effluent water treatment application is expected to witness the fastest growth rate of 5.1% on account of stringent wastewater disposal limitations imposed by the major international as well as regional regulatory bodies

• Raw treatment is also estimated to witness a notable growth rate. Due to the presence of suspended particles and heavy metals, the demand for pretreated industrial water is anticipated to increase especially in key countries such as the U.S., China, India, the UK, Germany, and Brazil

• During the forecasted years, it is anticipated that the presence of manufacturing facilities in the chemical, pharmaceutical, food & beverage, and automotive sectors in the U.S. and Canada would play a significant role in driving up demand for treatment services, thus triggering demand in the North America region

• Key players in the market are engaged in R&D activities coupled with mergers & acquisitions to gain a higher share of the market. For instance, Ecolab purchased Purolite a purification and separation life science solution provider in October 2021

Industrial Water Treatment Chemicals Market Segmentation

Grand View Research has segmented the global industrial water treatment chemicals market report based on the application and region:

Industrial Water Treatment Chemicals Application Outlook (Revenue, USD Million; Volume, Kilotons; 2018 - 2030)

• Raw Water Treatment

o Deoiling Polyelectrolytes (DOPE)

o Organic Coagulants

o Flocculants

o Filtration Aids

o Dewatering Aids

o Others

• Water Desalination

o Biocides

o Cleaning Agents

o Carbonates

o Sulfates

o Metal Oxides

o Silica

o Chelating Agents incl. NaOH

o Biofilms

o Others

o Antiscalants

o Flocculants

o Defoaming Agents

o Others

• Cooling & Boilers

o Sludge Controllers

o Antifoams

o Antiscalants

o Oxygen Scavengers

o Others

• Effluent Water Treatment

o Deoiling Polyelectrolytes (DOPE)

o Organic Coagulants

o Flocculants

o Filtration Aids

o Dewatering Aids

o Others

• Others

Industrial Water Treatment Chemicals Regional Outlook (Revenue, USD Million; Volume, Kilotons; 2018 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o Germany

o UK

o France

o Italy

o Spain

o Belgium

o Sweden

o Austria

o Finland

o Poland

o Turkey

• Asia Pacific

o China

o Japan

o South Korea

o India

o Singapore

o Indonesia

o Thailand

o Vietnam

o Australia

o New Zealand

o CIS

o Indonesia

o Rest of Asia Pacific

• Latin America

o Brazil

o Argentina

o Chile

• Middle East & Africa

o South Africa

Order a free sample PDF of the Industrial Water Treatment Chemicals Market Intelligence Study, published by Grand View Research.

#Industrial Water Treatment Chemicals Market#Industrial Water Treatment Chemicals Market Size#Industrial Water Treatment Chemicals Market Share#Industrial Water Treatment Chemicals Market Analysis#Industrial Water Treatment Chemicals Market Growth

0 notes

Text

Industrial Water Treatment Chemicals Market Growth, Drivers, and Key Insights

The global industrial water treatment chemicals market is witnessing significant growth as industries across the globe emphasize water conservation, regulatory compliance, and environmental sustainability. According to SkyQuest Technology, the market is anticipated to reach USD 21.23 billion by 2031, growing at a CAGR of 4.9% from 2024 to 2031. The rising demand for clean and treated water in industrial processes is driving the adoption of advanced water treatment solutions worldwide.

Market Drivers: What’s Powering the Growth?

Several factors are contributing to the growth of the industrial water treatment chemicals market:

Stringent Environmental Regulations Governments worldwide are enforcing strict regulations to limit industrial discharge of untreated wastewater, increasing the adoption of water treatment chemicals to comply with these laws.

Increasing Industrialization Rapid industrial growth, especially in developing economies, has intensified the need for effective water treatment to ensure efficient processes and reduce operational costs.

Rising Water Scarcity Growing concerns about freshwater scarcity are encouraging industries to recycle and reuse water through advanced treatment processes, boosting the demand for chemicals such as flocculants and coagulants.

Focus on Sustainable Practices Companies are increasingly adopting eco-friendly and biodegradable treatment chemicals to align with global sustainability goals.

Request a Sample Report - https://www.skyquestt.com/sample-request/industrial-water-treatment-chemicals-market

Key Market Segments: Breaking Down the Industry

The industrial water treatment chemicals market is categorized based on product type, end-use industry, and region:

1. By Product Type

Coagulants and Flocculants: Widely used in primary water treatment for removing solids and impurities.

Corrosion and Scale Inhibitors: Essential for maintaining pipeline integrity and preventing scaling in industrial equipment.

Biocides and Disinfectants: Used for controlling microbial growth in water systems.

pH Adjusters and Stabilizers: Maintain optimal pH levels for efficient treatment processes.

Others: Include anti-foaming agents, chelating agents, and oxidants.

2. By End-Use Industry

Power Generation: High water usage in cooling towers and boilers drives significant demand.

Oil & Gas: Treatment chemicals are used for water injection and refining processes.

Chemicals and Petrochemicals: Require large volumes of treated water for manufacturing.

Food & Beverage: Ensures water used in production meets strict hygiene standards.

Textiles: Water treatment is critical for dyeing and finishing processes.

Others: Includes paper & pulp, pharmaceuticals, and mining industries.

Speak to an Analyst - https://www.skyquestt.com/speak-with-analyst/industrial-water-treatment-chemicals-market

Regional Insights: A Global Perspective

North America

The North American market is driven by stringent environmental regulations and the need for efficient water management systems in industries like oil & gas, power, and manufacturing.

Europe

Europe’s focus on sustainability and the adoption of green chemicals is propelling the market. Countries like Germany, France, and the UK are leading in industrial water treatment innovations.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with rising industrialization in countries like China, India, and Southeast Asia driving demand. The region’s water scarcity issues further boost the adoption of advanced treatment chemicals.

Rest of the World

Regions such as the Middle East, Africa, and Latin America are witnessing growth due to expanding industries and increasing water reuse initiatives.

Top Companies in the Industrial Water Treatment Chemicals Market

The market is highly competitive, with leading companies focusing on innovation, sustainability, and strategic partnerships. Key players include:

Ecolab Inc.

BASF SE

Kemira Oyj

Suez S.A.

Kurita Water Industries Ltd.

The Dow Chemical Company

Solenis LLC

Ashland Global Holdings Inc.

Lonza Group AG

SNF Floerger

Buckman Laboratories International, Inc.

Veolia Water Technologies

AkzoNobel N.V.

GE Water & Process Technologies

NALCO (An Ecolab Company)

Make a Purchase Inquiry - https://www.skyquestt.com/buy-now/industrial-water-treatment-chemicals-market

Trends Shaping the Future of Water Treatment Chemicals

Development of Green Chemicals The industry is shifting towards biodegradable and sustainable water treatment chemicals to reduce environmental impact.

Automation and Digitization The adoption of IoT and AI in water treatment systems is enabling real-time monitoring and process optimization.

Focus on Water Reuse Growing investments in water recycling technologies are increasing the demand for advanced treatment chemicals.

Innovations in Chemical Formulations Companies are investing in R&D to develop multi-functional chemicals that offer enhanced performance.

The Road Ahead for Industrial Water Treatment Chemicals

The industrial water treatment chemicals market is poised for robust growth as industries continue to adopt sustainable practices and advanced technologies. With increasing water scarcity and stringent environmental norms, the demand for innovative treatment solutions will remain strong.

Leading companies are expected to focus on green innovations and strategic collaborations to meet the rising global demand for efficient water treatment chemicals.

Access the Full Report Here - https://www.skyquestt.com/report/industrial-water-treatment-chemicals-market

#Industrial Water Treatment Chemicals Market#Industrial Water Treatment Chemicals Market Size#Industrial Water Treatment Chemicals Market Share#Industrial Water Treatment Chemicals Market Trends#Industrial Water Treatment Chemicals Market Growth#Industrial Water Treatment Chemicals Market Outlook#Industrial Water Treatment Chemicals Market Overview#Industrial Water Treatment Chemicals Market Insights#Industrial Water Treatment Chemicals Market Forecast#Industrial Water Treatment Chemicals Market Analysis#Industrial Water Treatment Chemicals Market Statistics

0 notes

Text

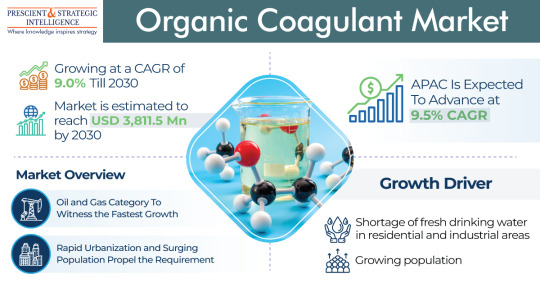

Harnessing Nature: Insights into the Organic Coagulant Market

The organic coagulant market is projected to reach at USD 3,811.5 million in 2030 with a CAGR of 9% in the years to come. The major reasons for this development of the industry are the scarcity of drinking and fresh water in residential and industrial areas along with the rising population, and urbanization.

And the rising demand for facilities like sewage treatment, industrial water treatment, fertilizer production, food & beverage industry, and paper manufacturing helps the demand for the chemical to grow.

And another major reason for the increasing demand is the growing population, which is creating an enormous demand for clean water and for which a need for advanced purification methods and also with the expansion of infrastructure for water treatment by government to meet the demand are all contributing the growth of eco-friendly water purification.

The oil & gas category will grow at a highest CAGR of 10% over the years, which is driven by the increasing use of organic chemicals with water at a required concentration for drilling and petroleum extraction purposes.

While, onshore and offshore operations both require different filtration processes as in onshore normal water is available, whereas offshore require advanced system to filter seawater. In addition, research and development activities are also contributing to the demand for organic coagulants, with eco-friendly solutions being explored for wastewater treatment.

Moreover, the increasing government focus to implement policies for water quality monitoring because of the increasing population all over the world. Strict regulations to prevent the direct release of harmful chemicals from industries and untreated sewage into water bodies.

APAC will grow the fastest in the organic coagulant market at a CAGR of 9.5% in the years to come due to the rapid urbanization and industrialization with rising population along with the rising investments in water treatment plant development and strict regulations on sewage disposal. Countries like India, China, South Korea, and Japan are expanding their contribution for the water treatment.

#organic coagulant#water treatment#wastewater treatment#coagulation solutions#eco-friendly chemicals#sustainable water treatment#natural coagulants#organic flocculants#water purification#organic coagulant applications#environmental sustainability#industrial water treatment#market growth#coagulation technology#organic chemicals

0 notes

Text

#Australia Water Treatment Chemicals Market#Australia Water Treatment Chemicals Market Size#Australia Water Treatment Chemicals Market Share#Australia Water Treatment Chemicals Market Analysis#Australia Water Treatment Chemicals Market Trends#Australia Water Treatment Chemicals Market Growth#Australia Water Treatment Chemicals Market Report#Australia Water Treatment Chemicals Market Research#Australia Water Treatment Chemicals Industry#Australia Water Treatment Chemicals Industry Report

0 notes

Text

The MEA Water & Waste Water Treatment Chemicals Market is projected to grow at around 5% CAGR during the forecast period, i.e., 2022-27. The growth of the market is likely to be driven by the rapidly increasing concerns over water contamination, improper treatment & disposal of waste from industries in water bodies, and the burgeoning demand for potable water by the rapidly growing population across the region.

#MEA Water & Waste Water Treatment Chemicals Market#MEA Water & Waste Water Treatment Chemicals Market growth#MEA Water & Waste Water Treatment Chemicals Market size#MEA Water & Waste Water Treatment Chemicals Market industry

0 notes

Text

Vacuum Priming Pumps Market Growth: Share, Value, Size, Trends, and Insights

"Vacuum Priming Pumps Market Size And Forecast by 2031

Global vacuum priming pumps market size was valued at USD 399.4 million in 2023 and is projected to reach USD 627.04 million by 2031, with a CAGR of 5.8% during the forecast period of 2024 to 2031.

the outlook for the Vacuum Priming Pumps Market remains optimistic, with significant opportunities for growth and innovation. The market’s competitive environment, shaped by leading companies and their strategies, underscores the importance of adaptability and foresight. With a focus on insights, trends, and data-driven analysis, this report serves as a comprehensive guide for stakeholders navigating the complexities of the Vacuum Priming Pumps Market.

Get a Sample PDF of Report - https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-vacuum-priming-pumps-market

Which are the top companies operating in the Vacuum Priming Pumps Market?

The Top 10 Companies in Vacuum Priming Pumps Market are known for their strong presence and innovative solutions. These include industry leaders. Each of these companies has made significant contributions through cutting-edge products, strategic partnerships, and global reach. Their ability to adapt to market trends and consumer demands has helped them maintain leadership positions in the market, driving growth and setting industry standards.

**Segments**

- By Type: Liquid Ring Vacuum Priming Pumps, Dry Vacuum Priming Pumps, Rotary Vane Vacuum Priming Pumps, Others - By End-User: Chemical Industry, Food and Beverage Industry, Oil and Gas Industry, Pharmaceutical Industry, Water Treatment Plants, Others - By Distribution Channel: Direct Sales, Indirect Sales

The global vacuum priming pumps market is segmented based on type, end-user, and distribution channel. In terms of type, the market is categorized into liquid ring vacuum priming pumps, dry vacuum priming pumps, rotary vane vacuum priming pumps, and others. Liquid ring vacuum priming pumps are widely used across various industries due to their efficient performance and durability. On the other hand, dry vacuum priming pumps are gaining popularity for their low maintenance requirements. The end-user segmentation includes the chemical industry, food and beverage industry, oil and gas industry, pharmaceutical industry, water treatment plants, and others. Different industries have distinct requirements for vacuum priming pumps, leading to a diverse range of applications. Distribution channels in the market consist of direct sales and indirect sales, with manufacturers focusing on expanding their reach through both channels to cater to a wide customer base.

**Market Players**

- Gardner Denver - Atlas Copco - Pfeiffer Vacuum - ULVAC, Inc. - Busch Vakuumpumpen und Systeme - Graham Corporation - KNF Neuberger GmbH - Tsurumi Manufacturing Co. Ltd. - Aqseptence Group - EBARA CORPORATION

Key market players in the global vacuum priming pumps market include Gardner Denver, Atlas Copco, Pfeiffer Vacuum, ULVAC, Inc., Busch Vakuumpumpen und Systeme, Graham Corporation, KNF Neuberger GmbH, Tsurumi Manufacturing Co. Ltd., Aqseptence Group, and EBARA CORPORATION. These companies are actively involved in research and development activities to introduce innovative technologies and enhance their product portfolios. Collaborations, partnerships, and acquisitions are common strategies adopted by these players to strengthen their market presence and expand their foothold in the industry. With a focus on developing energy-efficient and sustainable solutions, market players are driving advancements in vacuum priming pump technologies to meet evolving customer demands and regulatory requirements.

https://www.databridgemarketresearch.com/reports/global-vacuum-priming-pumps-marketThe global vacuum priming pumps market is witnessing significant growth driven by several key factors. One of the primary drivers is the increasing demand for efficient and reliable vacuum technologies across various industries such as chemical, food and beverage, oil and gas, pharmaceutical, and water treatment plants. These industries require vacuum priming pumps for a wide range of applications, including degassing, distillation, crystallization, and sterilization, among others. The growing emphasis on process optimization, operational efficiency, and product quality is further fueling the adoption of advanced vacuum priming pump solutions.

Moreover, technological advancements in vacuum priming pump design and performance are also contributing to market growth. Market players are investing in research and development activities to introduce innovative features such as improved energy efficiency, reduced maintenance requirements, and enhanced durability. These advancements are enabling end-users to achieve higher productivity levels, lower operating costs, and improved operational safety. Additionally, the ongoing focus on sustainability and environmental regulations is driving the demand for eco-friendly vacuum priming pump solutions that minimize carbon footprint and energy consumption.

Furthermore, the rising trend of industry 4.0 and automation in manufacturing processes is creating opportunities for the integration of smart technologies in vacuum priming pumps. Market players are increasingly incorporating IoT (Internet of Things), AI (Artificial Intelligence), and data analytics capabilities in their pump systems to enable real-time monitoring, predictive maintenance, and remote control functionalities. These smart features enhance operational efficiency, optimize resource utilization, and enable proactive decision-making in industrial settings.

In terms of market competition, key players such as Gardner Denver, Atlas Copco, Pfeiffer Vacuum, ULVAC, Inc., and others are focusing on strategic initiatives to strengthen their market position. These initiatives include product launches, partnerships, collaborations, and acquisitions to expand their product portfolios, geographic presence, and customer base. Additionally, the market is witnessing a growing trend of customization and specialization in vacuum priming pump solutions to meet specific end-user requirements and application needs.

Overall, the global vacuum priming pumps market is poised for steady growth driven by the increasing demand for efficient vacuum technologies across diverse industries, technological advancements in pump design, the emphasis on sustainability and environmental regulations, the integration of smart technologies, and strategic initiatives by key market players. These factors are expected to shape the future trajectory of the market and offer opportunities for innovation, growth, and market expansion in the coming years.**Segments**

Global Vacuum Priming Pumps Market Segmentation: - **By Type:** Gas liquid Mixed, Water Ring Wheel, and Jet Type - **By Application:** Environmental Protection, Agriculture, Industrial, Others

The global vacuum priming pumps market is characterized by a diverse range of product types and applications. Gas liquid mixed, water ring wheel, and jet type pumps cater to different industrial needs, providing solutions for applications in environmental protection, agriculture, industrial processes, and various other sectors. The versatility of these pump types allows for flexible usage across multiple industries, driving the market's growth and adoption rates.

**Market Players**

- KSB SE & Co. KGaA (Germany) - Calpeda S.p.A. (Italy) - Lowara S.r.l. (Italy) - Xylem Inc. (U.S.) - BBA Pumps B.V. (Netherlands) - DLT Thurott S.r.l. (Italy) - PSG, a Dover company (U.S.) - Brown Brothers Engineers (NZ) Ltd. (New Zealand) - Cornell Pump Company (U.S.) - The Gorman-Rupp Company (U.S.)

The global vacuum priming pumps market is further enriched by the presence of key players such as KSB SE & Co. KGaA, Calpeda S.p.A., Lowara S.r.l., Xylem Inc., BBA Pumps B.V., DLT Thurott S.r.l., PSG, Brown Brothers Engineers, Cornell Pump Company, and The Gorman-Rupp Company. These market players contribute significantly to the industry through their innovative technologies, diverse product portfolios, and strategic initiatives aimed at market expansion and customer satisfaction. With a focus on quality, efficiency, and sustainability, these companies drive advancements in vacuum priming pump solutions, meeting the dynamic needs of various industries and applications.

The global vacuum priming pumps market is poised for continuous growth, propelled by the increasing demand for efficient and reliable pumping solutions across diverse sectors. As industries prioritize operational excellence, product quality, and environmental sustainability, the market players are stepping up their efforts to deliver cutting-edge technologies that address these requirements. The integration of smart features, advancements in pump design, and a focus on customization are key factors shaping the market landscape, offering enhanced performance, energy efficiency, and operational safety to end-users.

Moreover, the market's competitive landscape is characterized by robust strategies employed by key players to solidify their market positions. Collaborations, acquisitions, product launches, and geographic expansions are key tactics utilized by market players to stay ahead in the competitive arena. This dynamic environment fosters innovation, fosters healthy competition, and underscores the industry's commitment to meeting evolving market demands. Overall, the global vacuum priming pumps market is on a trajectory of continuous growth, driven by technological advancements, industry trends, and strategic partnerships that enhance product offerings and market reach.

Explore Further Details about This Research Vacuum Priming Pumps Market Report https://www.databridgemarketresearch.com/reports/global-vacuum-priming-pumps-market

Key Insights from the Global Vacuum Priming Pumps Market :

Comprehensive Market Overview: The Vacuum Priming Pumps Market is growing rapidly, driven by technological advancements and evolving consumer preferences.

Industry Trends and Projections: The market is expected to grow at a CAGR of X% over the next five years, with increasing automation and digitalization.

Emerging Opportunities: New market segments, such as sustainable and eco-friendly solutions, are creating significant growth prospects.

Focus on R&D: Companies are investing heavily in R&D to innovate and improve product offerings, ensuring market leadership.

Leading Player Profiles: Major player dominate the market with strong portfolios and strategic partnerships.

Market Composition: The market is diverse, with a mix of large enterprises and emerging startups driving competition and innovation.

Revenue Growth: The market has witnessed a steady increase in revenue, primarily driven by growing demand and product diversification.

Commercial Opportunities: There are considerable opportunities for business expansion in emerging regions and through technological innovations.

Find Country based languages on reports:

https://www.databridgemarketresearch.com/jp/reports/global-vacuum-priming-pumps-markethttps://www.databridgemarketresearch.com/zh/reports/global-vacuum-priming-pumps-markethttps://www.databridgemarketresearch.com/ar/reports/global-vacuum-priming-pumps-markethttps://www.databridgemarketresearch.com/pt/reports/global-vacuum-priming-pumps-markethttps://www.databridgemarketresearch.com/de/reports/global-vacuum-priming-pumps-markethttps://www.databridgemarketresearch.com/fr/reports/global-vacuum-priming-pumps-markethttps://www.databridgemarketresearch.com/es/reports/global-vacuum-priming-pumps-markethttps://www.databridgemarketresearch.com/ko/reports/global-vacuum-priming-pumps-markethttps://www.databridgemarketresearch.com/ru/reports/global-vacuum-priming-pumps-market

Data Bridge Market Research:

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 975

Email:- [email protected]"

0 notes

Link

0 notes

Text

Industrial Chemical Distributor Chennai: Fulfilling Demand

Chennai, India's key industrial center, has a robust chemical industry. The need for quality industrial chemicals demands reliable distributors. They are intermediaries between suppliers and consumers, providing timely supply.

Role of an Industrial Chemical Distributor in Chennai

Distributors are lifelines for businesses requiring raw materials and specialty chemicals. Their functions are:

Sourcing: Collaborating with quality manufacturers for quality chemicals.

Storage and Logistics: Smooth delivery through well-managed warehouses.

Quality Control: Quality checks to achieve industry standards.

Regulatory Compliance: Ensuring chemicals conform to safety and environmental laws.

Technical Support: Offering advice on chemical handling and storage.

Types of Industrial Chemicals Available in Chennai

Basic Chemicals: Acids, alkalis, and solvents for production.

Specialty Chemicals: Adhesives, sealants, and performance-enhancers.

Pharmaceutical Chemicals: Raw materials for medicines and health products.

Agrochemicals: Fertilizers, pesticides, and growth regulators.

Construction Chemicals: Additives and waterproofing chemicals.

Water Treatment Chemicals: Coagulants and disinfectants for water treatment.

Advantages of Choosing a Reliable Industrial Chemical Distributor in Chennai

Consistent Quality Assurance: Certified suppliers guarantee high standards.

Diverse Product Portfolio: Wide range of chemicals for many industries.

Timely Delivery: Efficient supply chain management minimizes downtime.

Cost-Effective Solutions: Competitive bulk and customized chemical prices.

Sustainability and Safety: Ethical handling and sourcing of hazardous chemicals.

Industries Benefiting from Industrial Chemical Distributors in Chennai

Manufacturing and Processing Units: Require chemicals for production and maintenance.

Pharmaceutical and Healthcare Sector: Need high-purity chemicals for drugs.

Agriculture and Horticulture: Use agrochemicals to increase productivity and crop protection.

Construction and Infrastructure Development: Depend on construction chemicals for safety.

Water Treatment Facilities: Require chemicals for water purification and waste treatment.

How to Choose the Right Industrial Chemical Distributor in Chennai

Check Industry Experience: A veteran distributor offers reliability and experience.

Verify Product Quality: Ensure suppliers meet quality and regulatory requirements.

Assess Distribution Network: A strong logistics network ensures on-time delivery.

Compare Pricing and Availability: Competitive pricing and readiness to stock are essential.

Evaluate Customer Support: Technical support adds value to service.

Conclusion

A reliable industrial chemical distributor Chennai is vital for smooth operations across industries. They offer high-quality chemicals, experience, and compliance, enabling efficiency and innovation. Chennai's industrial sector thrives with dependable distributors meeting market demands.

0 notes

Text

Chitosan Market Rapidly Growing With Strong Demand In Healthcare And Personal Care Products

The chitosan market is witnessing substantial growth due to its diverse applications in pharmaceuticals, agriculture, cosmetics, and water treatment. With the increasing demand for biodegradable and eco-friendly materials, chitosan is becoming a preferred choice in multiple industries. The following are key market drivers contributing to its rapid expansion.

Increasing Demand For Biodegradable Alternatives

Growing awareness regarding environmental pollution is pushing industries towards biodegradable materials

chitosan is a natural and sustainable alternative to synthetic polymers, making it highly desirable

Rising government regulations on plastic usage are accelerating the shift towards eco-friendly materials

Industries such as packaging, textiles, and food processing are adopting chitosan-based biodegradable products

Expanding Use In Pharmaceutical Industry

chitosan is used for drug delivery systems due to its bioadhesive and controlled-release properties

Antimicrobial and wound-healing properties make it an essential ingredient in medical bandages and tissue engineering

Ongoing research is exploring chitosan-based solutions for cancer treatment and vaccine delivery

The pharmaceutical sector is leveraging chitosan for its ability to enhance drug solubility and bioavailability

Growing Application In Water Treatment Solutions

chitosan is a highly effective agent for removing heavy metals and contaminants from water

Industrial wastewater treatment plants are incorporating chitosan due to its non-toxic nature

Increasing global concerns about water pollution are driving demand for sustainable treatment solutions

Cost-effective and efficient performance makes chitosan a preferred choice for municipal water treatment facilities

Rising Demand In The Agriculture Sector

chitosan-based biofertilizers enhance soil fertility and plant growth, reducing the dependency on chemical fertilizers

Acts as a natural plant growth regulator, improving crop yield and resistance to diseases

Used in seed coating to improve germination rates and crop protection against pests

Increasing demand for organic farming is driving the use of chitosan-based agricultural inputs

Expanding Applications In The Food Industry

chitosan is widely used as a natural preservative in food processing due to its antimicrobial properties

Helps in extending the shelf life of perishable food products by preventing microbial growth

Used in edible films and coatings to maintain food freshness and prevent contamination

Growing consumer preference for natural food additives is boosting chitosan adoption in food packaging

Increasing Use In Cosmetics And Personal Care Products

chitosan is used in skincare products for its moisturizing and anti-aging benefits

Acts as a natural film-forming agent, improving the texture and stability of cosmetic formulations

Growing demand for organic and chemical-free beauty products is fueling the use of chitosan in cosmetics

Used in hair care products for its ability to strengthen hair and improve scalp health

Rising Investments In Research And Development

Continuous innovation in chitosan-based nanotechnology is opening new market opportunities

Ongoing studies are exploring chitosan applications in tissue engineering and regenerative medicine

Pharmaceutical and biotechnology companies are heavily investing in chitosan-based drug formulations

The emergence of chitosan-based bioplastics is attracting investments from sustainable packaging firms

Supportive Government Regulations And Policies

Many countries are implementing policies that promote the use of biodegradable and renewable materials

Government incentives for research on bio-based materials are fostering innovation in the chitosan industry

Stringent regulations on synthetic chemicals are pushing industries towards natural alternatives like chitosan

Support for sustainable agricultural practices is encouraging the adoption of chitosan-based fertilizers and pesticides

Rising Awareness About Health Benefits

chitosan is gaining popularity as a dietary supplement for weight management and cholesterol control

Known for its ability to bind to fats and prevent their absorption in the digestive system

Increasing consumer preference for functional foods and nutraceuticals is boosting chitosan demand

Used in dietary supplements to enhance gut health and improve overall metabolic functions

Advancements In Manufacturing Technologies

Improved extraction and purification methods are reducing the production cost of chitosan

Development of fungal-derived chitosan is addressing raw material scarcity and sustainability concerns

Advanced processing techniques are enhancing the quality and consistency of chitosan products

Integration of automation in production facilities is increasing efficiency and reducing manufacturing waste

Growing Demand From The Textile Industry

chitosan is used as a sustainable alternative in textile finishing for antibacterial and odor-resistant fabrics

Textile manufacturers are incorporating chitosan to enhance fabric durability and moisture-wicking properties

Increasing demand for eco-friendly clothing is driving the adoption of chitosan-based textile treatments

Its biodegradability aligns with the global trend towards sustainable fashion and ethical manufacturing

Increasing Adoption In Veterinary And Animal Health

chitosan is used in animal feed additives to enhance gut health and immunity in livestock

Veterinary medicine is utilizing chitosan for wound healing and infection control in animals

Growing awareness about sustainable animal husbandry is encouraging the use of chitosan in pet nutrition

Its antimicrobial properties help in disease prevention and overall animal welfare

Expansion Of Global Supply Chain And Trade

The rising international trade of chitosan products is facilitating market expansion across regions

Increasing collaborations between manufacturers and research institutions are driving technological advancements

Emerging economies are witnessing rapid industrialization, creating new growth avenues for the chitosan industry

The establishment of new processing plants and production facilities is strengthening supply chains

Growing Use In 3D Bioprinting And Biomedical Applications

chitosan-based bio-inks are revolutionizing 3D bioprinting for tissue engineering applications

Used in regenerative medicine to create biocompatible scaffolds for cell growth and tissue repair

Its ability to mimic the extracellular matrix makes it an ideal material for artificial organ development

Ongoing advancements in biomaterials are expanding the scope of chitosan in the healthcare sector

Surge In Demand From The Paints And Coatings Industry

chitosan-based coatings are being developed for their antimicrobial and corrosion-resistant properties

Used in protective coatings for medical devices, food packaging, and industrial equipment

The rise in demand for sustainable and eco-friendly coatings is propelling the use of chitosan in this sector

Innovation in smart coatings incorporating chitosan for self-healing and functional properties is gaining traction

0 notes

Text

Compression Coupling Market Growth, Supply Demand by 2024-2032

The Reports and Insights, a leading market research company, has recently releases report titled “Compression Coupling Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2024-2032.” The study provides a detailed analysis of the industry, including the global Compression Coupling Market share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Compression Coupling Market?

The compression coupling market is expected to grow at a CAGR of 3.9% during the forecast period of 2024 to 2032.

What are Compression Coupling?

A compression coupling is a plumbing fitting utilized to connect two pipes or tubes. It comprises a compression nut, a compression ring (or ferrule), and the coupling body. Pipes are inserted into each end of the coupling, and the compression nut is tightened onto the body, compressing the ring to create a watertight seal between the pipes. These couplings are popular in plumbing for their simple installation and ability to form a secure connection without soldering or welding.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/1745

What are the growth prospects and trends in the Compression Coupling industry?

The compression coupling market growth is driven by various factors and trends. The market for compression couplings is experiencing consistent growth, fueled by the rising demand for dependable and easy-to-use plumbing solutions. These couplings are favored for their ability to establish a secure and leak-proof connection between pipes without requiring soldering or welding. They find extensive application in plumbing systems across residential, commercial, and industrial sectors. The market offers a diverse range of products, including brass, copper, and plastic couplings, tailored to various needs and preferences. Noteworthy trends in the market include the introduction of innovative coupling designs to enhance performance and longevity, alongside the growing adoption of eco-friendly materials. Hence, all these factors contribute to compression coupling market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

By Product Type:

Straight Couplings

Transition Couplings

Reduced Couplings

Repair Couplings

Expansion Couplings

Others

By End-Use Industry:

Plumbing

HVAC (Heating, Ventilation, and Air Conditioning)

Oil and Gas

Chemical and Petrochemical

Water and Wastewater Treatment

Mining

Agriculture

Others

By Application:

Water Distribution

Gas Distribution

Industrial Fluid Transfer

Irrigation Systems

Sewer and Drainage Systems

Fire Protection Systems

Others

Segmentation By Region:

North America:

United States

Canad

Europe:

Germany

The U.K.

France

Spain

Italy

Russia

Poland

BENELUX

NORDIC

Rest of Europe

Asia Pacific:

China

Japan

India

South Korea

ASEAN

Australia & New Zealand

Rest of Asia Pacific

Latin America:

Brazil

Mexico

Argentina

Middle East & Africa:

Saudi Arabia

South Africa

United Arab Emirates

Israel

Who are the key players operating in the industry?

The report covers the major market players including:

Victaulic Company

Mueller Water Products

Uponor Corporation

Georg Fischer Piping Systems Ltd.

McWane Inc.

Reed Manufacturing Company

Fernco Inc.

Anvil International

Smith-Blair Inc.

NIBCO Inc.

Romac Industries, Inc.

Tyco International Ltd.

Matco-Norca Inc.

View Full Report: https://www.reportsandinsights.com/report/Compression Coupling-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients globally.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd. 1820 Avenue M, Brooklyn, NY, 11230, United States Contact No: +1-(347)-748-1518 Email: [email protected] Website: https://www.reportsandinsights.com/ Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/ Follow us on twitter: https://twitter.com/ReportsandInsi1

#Compression Coupling Market share#Compression Coupling Market size#Compression Coupling Market trends

0 notes

Text

Global Nanobubbles Market Report 2025: Growth Trends, Drivers, and Future Prospects

Introduction

The global nanobubbles market is rapidly expanding as industries adopt nanobubble technology for enhanced efficiency and sustainability. Nanobubbles—extremely small gas bubbles with unique properties—are being used across various sectors, including water treatment, agriculture, healthcare, and aquaculture. This report offers key insights into the market, covering growth trends, drivers, challenges, regional dynamics, and future forecasts.

If you’re exploring nanobubble technology, this comprehensive guide will provide valuable information on the market’s potential.

Market Overview

The nanobubbles market is projected to reach $1.8 billion by 2030, growing at a CAGR of 8.5% from 2023 to 2030. The rising demand for sustainable solutions in water treatment, agriculture, and industrial applications is a key factor driving this growth.

What are Nanobubbles?

Nanobubbles, also known as ultrafine bubbles, are gas bubbles smaller than 200 nanometers in diameter. Unlike conventional bubbles, nanobubbles remain suspended in liquid for long periods and have high surface area, leading to unique properties such as enhanced oxygen transfer and surface cleaning.

Key Applications

Water Treatment – Nanobubbles improve oxygenation, reduce chemical usage, and enhance water quality.

Agriculture – Used for increasing crop yield, improving soil health, and reducing fertilizer requirements.

Aquaculture – Improve water quality, oxygenation, and disease prevention in fish farming.

Healthcare – Emerging applications in wound healing, cancer treatment, and drug delivery.

Food & Beverage – Used for cleaning, sterilization, and improving product quality.

Key Market Drivers

Rising Demand for Sustainable Water Treatment Solutions

Stringent regulations on water quality and growing environmental concerns are driving the adoption of nanobubble technology in water treatment.

Increasing Applications in Agriculture and Aquaculture

Nanobubbles enhance plant growth, improve nutrient absorption, and reduce water usage, making them an ideal solution for sustainable farming.

In aquaculture, nanobubbles reduce fish mortality and improve overall yield.

Technological Advancements in Nanobubble Generation

Continuous innovation in nanobubble generation systems is expanding their use across industries.

Compact, energy-efficient nanobubble generators are becoming more accessible and affordable.

Growing Interest in Health and Wellness

The healthcare sector is exploring new applications of nanobubbles for oxygen therapy and drug delivery, presenting significant growth opportunities.

Regional Insights

North America

North America leads the nanobubbles market due to the widespread adoption of advanced water treatment technologies and strong government regulations on environmental protection. The U.S. is the largest contributor in the region.

Europe

Europe is witnessing growing demand for nanobubbles in agriculture and aquaculture. Countries like Germany, the Netherlands, and Norway are investing in sustainable farming and fishery practices that rely on nanobubble technology.

Asia-Pacific

Asia-Pacific is the fastest-growing region, driven by rising industrialization, water scarcity concerns, and increasing adoption of nanobubbles in agriculture and aquaculture. China, India, and Japan are leading markets in this region.

Middle East & Africa

The Middle East focuses on water management and desalination projects, driving the demand for nanobubble technology in water treatment applications.

Leading Players in the Nanobubbles Market

The nanobubbles market is highly innovative, with several companies focusing on R&D and expanding their technology offerings. Key players include:

Moleaer Inc.

Nano Gas Technologies

AquaB Nanobubble Innovations

Ecologix Environmental Systems

Hollitech

Infracore Company Ltd.

These companies are investing in strategic collaborations, partnerships, and new product launches to expand their market presence.

Challenges in the Nanobubbles Market

High Initial Investment Costs: The installation of nanobubble systems can be costly, limiting adoption in some regions.

Limited Awareness and Understanding: Despite its benefits, nanobubble technology is still relatively unknown to many industries.

Regulatory and Technical Barriers: Complex regulations and lack of standardized protocols can pose challenges in certain markets.

Future Outlook

The future of the nanobubbles market is promising, with increasing investments in research and development. Emerging applications in healthcare, biomedicine, and advanced manufacturing will further expand the market. Key future trends include:

Integration with IoT and Smart Water Management Systems

Expansion into Biotech and Pharmaceuticals

Development of Portable and Energy-Efficient Nanobubble Generators

Growing Use in Carbon Sequestration and Climate Change Mitigation Projects

Conclusion

The global nanobubbles market is at an exciting stage of growth, with expanding applications across diverse industries. As the demand for sustainable, high-performance solutions increases, nanobubble technology is expected to play a crucial role in addressing global challenges in water management, agriculture, and healthcare.

Looking for strategic insights into the nanobubbles market? Mark & Spark Solutions offers tailored market research and business solutions to help you navigate emerging opportunities.

Visit Mark & Spark Solutions for customized insights and expert advice.

0 notes

Text

Europe Anti-condensation Masterbatch Market, Outlook and Forecast 2025-2030

Anti-condensation masterbatch refers to polymer additives specifically designed to prevent condensation from forming on plastic surfaces. These additives are commonly incorporated into plastic films and sheets used in agricultural, packaging, and construction applications. Modern formulations of anti-condensation masterbatches offer long-lasting effectiveness by altering the surface energy of plastics, ensuring that water droplets spread evenly into a thin, transparent layer rather than forming visible droplets that can obscure visibility and affect product integrity.

Download FREE Sample of this Report @ https://www.24chemicalresearch.com/download-sample/285570/europe-anticondensation-masterbatch-forecast-market-2025-2030-303

Market Size

The Europe Anti-condensation Masterbatch market was valued at US$ 132.46 million in 2024 and is projected to reach US$ 185.62 million by 2030, growing at a CAGR of 5.78% during the forecast period of 2024-2030. This growth is driven by increasing demand in agricultural films, where condensation control is critical for maintaining light transmission and preventing crop diseases. The agricultural film segment holds a 45.6% market share, followed by packaging (32.4%) and construction (12.8%). Technological advancements have improved efficiency by 35.6%, while R&D investments in the sector amounted to approximately €38.4 million in 2023.

Market Dynamics (Drivers, Restraints, Opportunities, and Challenges)

Drivers

Growth in Agricultural Applications – The adoption of greenhouse films with anti-condensation properties is rising due to their ability to improve crop yield and reduce plant diseases.

Expanding Packaging Industry – Anti-condensation masterbatch is increasingly used in food packaging films to prevent moisture accumulation, enhancing product visibility and shelf-life.

Advancements in Polymer Additives – The development of more efficient and long-lasting anti-condensation masterbatches is driving product adoption across various sectors.

Stringent European Regulations – Regulations promoting sustainable packaging and high-performance plastic materials contribute to the rising demand for specialized masterbatches.

Restraints

High Production Costs – The cost of high-quality polymer additives increases the overall price of anti-condensation masterbatch, limiting its adoption in cost-sensitive markets.

Environmental Concerns – The use of certain chemical additives in plastics faces scrutiny due to environmental impact concerns, leading to regulatory challenges.

Limited Awareness Among Small-Scale Users – While large agricultural and packaging companies are adopting anti-condensation solutions, awareness among small-scale users remains low.

Opportunities

Development of Bio-based Anti-condensation Masterbatches – Growing interest in sustainable plastic additives presents an opportunity for manufacturers to develop eco-friendly alternatives.

Expanding Applications in Construction Films – The increasing use of plastic sheets with condensation control in buildings and greenhouses creates new growth avenues.

Technological Innovations in Polymer Chemistry – Advanced formulations with improved longevity and performance are expected to boost market penetration.

Challenges

Raw Material Price Fluctuations – The cost of polymer resins and additives impacts the overall production costs, creating pricing uncertainties.

Competition from Alternative Technologies – Nanocoatings and hydrophilic surface treatments present alternative solutions, posing a competitive challenge.

Supply Chain Disruptions – Issues such as transportation delays and raw material shortages affect market stability.

Regional Analysis

Germany

Germany leads the European market due to its strong industrial base, technological innovations, and high demand in agricultural and packaging applications.

United Kingdom

The UK sees steady growth in anti-condensation masterbatch demand, particularly in high-quality food packaging and sustainable plastic solutions.

France

France's packaging sector, driven by stringent food safety regulations, is a key contributor to market expansion.

Italy & Spain

Both countries are witnessing increased adoption in agricultural films due to their extensive greenhouse farming practices.

Netherlands & Belgium

These regions are investing in advanced polymer additives, making them emerging hotspots for market growth.

Competitor Analysis

Key Players

Clariant AG – Leading provider with a strong focus on sustainable masterbatches.

PolyOne Corporation – Known for high-performance polymer solutions.

Ampacet Corporation – Offers a diverse portfolio of anti-condensation masterbatches.

LyondellBasell Industries N.V. – Focuses on innovative polymer technologies.

Plastika Kritis S.A. – Specializes in masterbatches for agricultural applications.

Tosaf Group – Provides advanced additive solutions.

Penn Color, Inc. – Expertise in color and additive masterbatches.

A. Schulman, Inc. – Offers a broad range of plastic additives.

Fraunhofer Institute – Involved in research and development of next-generation polymer additives.

Croda International Plc – Focused on sustainable and high-performance additives.

Market Segmentation (by Application)

Film

Sheet

Other

Market Segmentation (by Type)

Glyceryl Ester Based

Other

Key Company

Retain this section intact as per the guidelines.

Geographic Segmentation

Retain this section intact as per the guidelines.

FAQs

What is the current market size of the Europe Anti-condensation Masterbatch market?

➣ The market was valued at US$ 132.46 million in 2024 and is projected to reach US$ 185.62 million by 2030 at a CAGR of 5.78%.

Which are the key companies operating in the Europe Anti-condensation Masterbatch market?

➣ Key players include Clariant AG, PolyOne Corporation, Ampacet Corporation, LyondellBasell Industries N.V., Plastika Kritis S.A., Tosaf Group, Penn Color, Inc., A. Schulman, Inc., Fraunhofer Institute, and Croda International Plc.

What are the key growth drivers in the Europe Anti-condensation Masterbatch market?

➣ The market is driven by growth in agricultural applications, expanding packaging industry, advancements in polymer additives, and stringent European regulations promoting high-performance plastics.

Which regions dominate the Europe Anti-condensation Masterbatch market?

➣ Germany holds the largest market share at 35.4%, followed by the UK, France, Italy, Spain, Netherlands, and Belgium.

What are the emerging trends in the Europe Anti-condensation Masterbatch market?

➣ Emerging trends include bio-based masterbatches, expanding applications in construction films, and technological innovations in polymer chemistry.

Competitor Analysis

The report also provides analysis of leading market participants including:

Key companies Anti-condensation Masterbatch revenues in Europe market, 2019-2024 (Estimated), ($ millions)

Key companies Anti-condensation Masterbatch revenues share in Europe market, 2023 (%)

Key companies Anti-condensation Masterbatch sales in Europe market, 2019-2024 (Estimated),

Key companies Anti-condensation Masterbatch sales share in Europe market, 2023 (%)

Key Points of this Report:

The depth industry chain includes analysis value chain analysis, porter five forces model analysis and cost structure analysis

The report covers Europe and country-wise market of Anti-condensation Masterbatch

It describes present situation, historical background and future forecast

Comprehensive data showing Anti-condensation Masterbatch capacities, production, consumption, trade statistics, and prices in the recent years are provided

The report indicates a wealth of information on Anti-condensation Masterbatch manufacturers

Anti-condensation Masterbatch forecast for next five years, including market volumes and prices is also provided

Raw Material Supply and Downstream Consumer Information is also included

Any other user's requirements which is feasible for us

Reasons to Purchase this Report:

Analyzing the outlook of the market with the recent trends and SWOT analysis

Market dynamics scenario, along with growth opportunities of the market in the years to come

Market segmentation analysis including qualitative and quantitative research incorporating the impact of economic and non-economic aspects

Regional and country level analysis integrating the demand and supply forces that are influencing the growth of the market.

Market value (USD Million) and volume (Units Million) data for each segment and sub-segment

Distribution Channel sales Analysis by Value

Competitive landscape involving the market share of major players, along with the new projects and strategies adopted by players in the past five years

Comprehensive company profiles covering the product offerings, key financial information, recent developments, SWOT analysis, and strategies employed by the major market players

1-year analyst support, along with the data support in excel format.

Download FREE Sample of this Report @ https://www.24chemicalresearch.com/download-sample/285570/europe-anticondensation-masterbatch-forecast-market-2025-2030-303

0 notes

Text

Soda Ash Market Key Drivers of Increased Demand and Innovation

Soda ash, or sodium carbonate, is a critical industrial chemical with a wide range of applications, including glass manufacturing, detergents, chemicals, and water treatment. The soda ash market has seen consistent growth over the past few years, driven by several key factors. These drivers are shaping the future of the market and fostering opportunities for manufacturers and suppliers worldwide. In this article, we will explore the primary drivers fueling the growth of the soda ash market and how these trends are expected to impact the industry.

1. Increased Demand from the Glass Industry

The glass industry is the largest consumer of soda ash, accounting for more than 50% of global demand. Soda ash is essential in the production of various types of glass, including flat glass, container glass, and fiberglass. With the increasing demand for glass products in construction, automotive, electronics, and consumer goods industries, the soda ash market continues to expand.

One of the most significant drivers is the global rise in urbanization and infrastructure development. As countries in Asia-Pacific, the Middle East, and Africa continue to urbanize, the demand for glass in buildings, transportation, and consumer products grows. Additionally, energy-efficient technologies, such as low-emissivity glass, which helps reduce heating and cooling costs, are contributing to a higher demand for soda ash as it is a key ingredient in the production of such glass.

2. Industrial Growth in Emerging Economies

Emerging economies, particularly in Asia, are witnessing rapid industrial growth, which has led to an increase in demand for various chemicals, including soda ash. In regions like China, India, and Southeast Asia, the demand for soda ash has surged due to increased manufacturing activities in sectors such as textiles, chemicals, detergents, and construction materials.

As industries expand and infrastructure development accelerates in these regions, the demand for products that require soda ash, such as detergents, chemicals, and glass, continues to rise. The growing middle class in these countries is also contributing to the increased consumption of consumer goods that require packaging made from glass and chemicals, further driving the demand for soda ash.

3. Growth in the Detergent and Chemical Industries

Soda ash is a key ingredient in the production of detergents, especially laundry detergents, which are widely used in households and industries. With the growing population and rising disposable incomes, the demand for cleaning and household products has skyrocketed, particularly in emerging markets. The detergent industry alone accounts for a significant portion of global soda ash consumption, and as demand continues to increase, soda ash consumption is expected to follow suit.

Additionally, soda ash is crucial in the manufacturing of various chemicals, such as sodium bicarbonate, sodium silicate, and other chemicals used in industrial processes. As the global chemical industry expands, particularly in the Asia-Pacific and Latin American regions, the need for soda ash as a raw material is growing, making it a critical driver for the market.

4. Sustainability and Environmental Regulations

Sustainability has become a key focus in global industries, and the soda ash market is no exception. As industries strive to meet stricter environmental regulations and reduce their carbon footprints, sustainable production methods have gained importance. For instance, soda ash manufacturers are increasingly adopting energy-efficient production processes and recycling methods to reduce emissions and minimize waste.

Furthermore, regulations around water treatment and waste management are also boosting the demand for soda ash. In water softening and wastewater treatment, soda ash plays an important role in neutralizing water acidity and removing impurities. As governments worldwide impose stricter water quality standards, the use of soda ash in water treatment processes is expected to increase, thereby driving market growth.

5. Technological Advancements in Production

Technological innovation in soda ash production has significantly improved efficiency, product quality, and environmental sustainability. Traditional production methods such as the Solvay process and the ammonia-soda process have evolved to become more energy-efficient and cost-effective. New technologies are helping manufacturers reduce operational costs, increase yields, and decrease carbon emissions.

For example, advancements in the use of renewable energy sources and carbon capture technologies are reducing the environmental impact of soda ash production. These innovations not only improve the sustainability of soda ash production but also help reduce the overall cost of manufacturing, making the product more competitive in the market.

As these technologies continue to evolve, the production of soda ash becomes more environmentally friendly, which aligns with global trends towards greener industrial practices and increases the attractiveness of soda ash in environmentally conscious markets.

6. Expansion of Soda Ash Applications

The versatility of soda ash continues to drive market growth, as its applications expand beyond traditional sectors such as glass manufacturing and detergents. Soda ash is increasingly used in industries like chemicals, textiles, food processing, and even agriculture. For example, soda ash is used in the production of sodium bicarbonate, a widely used compound in the food and pharmaceutical industries.

In addition, the use of soda ash in the production of various chemical intermediates, such as sodium silicate, has risen with the growth of industrial activities worldwide. The growing demand for soda ash in these non-glass applications, coupled with its cost-effectiveness and availability, is further driving its market growth.

7. Increased Focus on Water Treatment

Water scarcity and contamination are critical challenges faced by many regions worldwide. To address these issues, water treatment has become a priority for governments and organizations across the globe. Soda ash is a key ingredient in water treatment processes, particularly in softening hard water and neutralizing acidic water.

With the growing emphasis on improving water quality and ensuring safe drinking water, soda ash is increasingly being used in water purification and wastewater treatment systems. The need for more efficient and eco-friendly water treatment processes, especially in emerging economies, is likely to drive significant demand for soda ash in the coming years.

Conclusion

The soda ash market is experiencing growth driven by multiple factors, including rising demand from the glass industry, industrial expansion in emerging markets, and increased use in detergent and chemical manufacturing. Technological advancements in production processes and the growing emphasis on sustainability and water treatment further contribute to the market's positive outlook. As industries continue to evolve, the demand for soda ash will likely continue to rise, providing opportunities for growth in both developed and emerging markets. Manufacturers who can capitalize on these drivers and embrace new innovations will be well-positioned to succeed in the competitive soda ash market.

0 notes

Text

The GCC Water & Waste Water Treatment Chemicals Market is projected to grow at a CAGR of around 18.2% during the forecast period, i.e., 2023-2028, says MarkNtel Advisors. The market growth primarily attributes to the increasing issues of water contamination, burgeoning waste from industries, which gets discharged in water bodies, and mounting need for potable water due to rapid industrialization & expansion across the Gulf countries.

#GCC Water & Waste Water Treatment Chemicals Market#GCC Water & Waste Water Treatment Chemicals Market growth#GCC Water & Waste Water Treatment Chemicals Market size#GCC Water & Waste Water Treatment Chemicals Market industry

0 notes

Link

0 notes

Text

Chemical Manufacturing Company in Chennai: A Growing Industrial Hub

Chennai emerges as a major industrial centre in India where chemical manufacturing activities have become prominent. The increasing number of chemical manufacturing company in Chennai benefits from a strong infrastructure base and experienced workers and advantageous port access. Industry players supply premium chemicals that serve pharmaceuticals as well as agriculture and textiles and construction activities.

Importance of Chemical Manufacturing in Chennai

The chemical industry supports various national industries through its production of fundamental raw materials and special-purpose chemical blends. The chemical industry in Chennai thrives due to public backing combined with research facilities and dependable logistics systems which make it an ideal place for chemical manufacturing.

Types of Chemicals Manufactured in Chennai

The production sector employs industrial chemicals which serves both manufacturing operations and industrial cleaning procedures and industrial coverings.

Pharmaceutical Chemicals: Active pharmaceutical ingredients (APIs) and excipients for drug formulation.

Agrochemicals: Fertilizers, pesticides, and soil conditioners for enhanced agricultural productivity.

Specialty Chemicals: Customized solutions for industries such as textiles, paper, and water treatment.

Petrochemicals serve as important raw materials to create plastics while providing base materials for rubber manufacturing together with synthetic fibres production.

Construction Chemicals provide sealants and adhesives with waterproofing solutions which extend the longevity of buildings.

Advantages of Choosing a Chemical Manufacturing Company in Chennai

Quality Assurance: Companies adhere to stringent quality control measures and global standards.

Buyers profit from cost-efficient solutions because pricing remains competitive along with manufacturing processes that deliver high efficiency.

Research and development innovations are driven through advanced laboratories which operate with skilled researchers.

The adoption of environmentally friendly manufacturing approaches has become common practice among multiple production facilities.

The logical backbone of Chennai consists of meticulously developed transportation facilities that deliver chemicals promptly.

Industries Benefiting from Chemical Manufacturing in Chennai

The Pharmaceutical Industry demands bulk chemicals as fundamental ingredients to create medications along with their medical applications.

Agrochemicals in agriculture provide farmers with two benefits that include higher crop yields and pest defense capabilities.

Automobile and Aerospace Industry: Relies on high-performance coatings and lubricants.

Specialty chemicals enable fabric treatment while performing dyeing operations in the Textile and Dyeing industry.

Food and Beverage industry applies food-grade chemicals and preservatives which increase shelf life of their products.

How to Choose the Right Chemical Manufacturing Company in Chennai

Verify that the business abides by regulatory guidelines as well as safety standards.

The availability of many chemical products provides evidence of a company's expertise level and product reliability.

A thorough evaluation must be made to assess research and development capabilities since formulations need innovative approaches and customization features.

A company must offer competitive prices along with efficient distribution services to excel in the market.

Technical support together with strong after-sales services creates additional value which strengthens an association between businesses.

Conclusion

Industrial growth in the Chennai area receives substantial support from the local chemical manufacturing operations. High-quality chemical solutions delivered by these companies serve various industries by meeting industry standards for efficiency and sustainability. The increasing demand keeps Chennai as the main choice for chemical manufacturing and supply activities which strengthens industrial development and economic expansion.

0 notes